Retirement – sounds so final, doesn’t it? You’re not getting there. Not the way you think. Or not the way you thought. Remember the days of company financed pensions? Yeah, neither do I.

This post contains affiliate links.

What, no pension?

Generally speaking, pensions are a thing of the past, given their inherent lack of sustainability. Pensions – any kind of annuity requires significant contributions from the bottom of the pyramid filtering to the top. The Gargantuan Ponzi Scheme otherwise known as Social Security should have taught us that. If one is risk adverse, then saving for retirement has become nearly futile.

Let me explain: in my parent’s generation, the “floor” was 5%. If you didn’t want to risk the stock market, invest in corporate bonds, options, or futures, there was always the savings banks with their FDIC. There were also U.S. Treasury Securities and Certificates of Deposit if you could afford to park your money long term.

Weren’t we told to be thrifty?

Our parents or grand-parents, having spent their formative years in the Great Depression would go on about the “power of interest.” Sure one could make a fortune in the markets or by starting a business. One could also lose everything. So our parents settled onto the steady, solid middle-class ground of their savings bank accounts. And the always reliable power of interest.

A married couple starting out at the age of 25 making deposits of $875 a month each month until they reach 60, assuming a modest interest rate of 5% would end up with 1 million dollars in savings. If they were disciplined. If they exercised thrift. In other words, if they employed the single most important factor in accumulating wealth: delayed gratification.

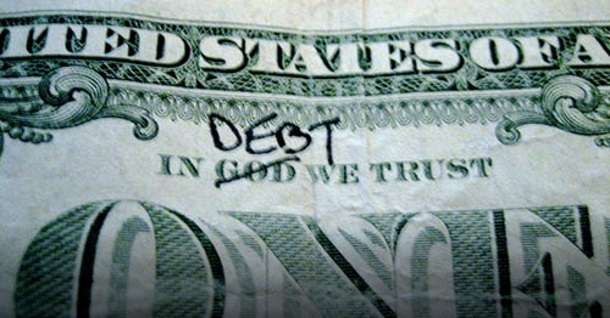

Then in 1982, something happened which would affect the world of finance up to this day. The national debt of the United States government reached 1 trillion dollars. Imagine a stack of $10 bills reaching into low-Earth orbit. That’s a trillion dollars. To make the debt manageable, interest rates had to come down. Inflation slowed to crawl. After the economic insanity of the 70s, this was seen as a good thing.

Mutual Funds became all the rage, spreading out the risk in stocks and corporate bonds. Fueled by massive debt, the economy roared, but month by month, interest rates ticked downward. CDs and treasury securities, once paying off in the double digits, spiraled downward. By the 90s, CDs were paying what savings accounts used to. The 21st century saw “negative interest rates” – the bizarre circumstance of the Federal Reserve lending money to banks below the rate of inflation.

Condescended to by amateurs.

Under Barrak Obama’s watch, more money will have been added to the national debt than under the previous 43 administration combined. As surely as Nemesis follow Hubris, any idea that the laws of economics could be overcome by sheer force of will is a special kind of absurdity.

I refuse to accept your reality. This MUST be a door.

Is this his fault? Only in part. Just as no single raindrop thinks its responsible for the flood that destroys the town, not a single one of our public officials will every take responsibility for the untenable circumstance in which we find ourselves.

The nation experienced an ill-timed financial re-alignment which began in the Fall of 2008 (can we please dispense with the shrieking drama of calling it a “crisis?”). Ill-timed because it paved the way for the most unprepared candidate in the history of the republic to assume the presidency. And it showed over the course of the next 8 years. Economic theoreticians of the administration in cooperation with a compliant congress borrowed over 10 trillion dollars.

Any parallels between this administration and the 80s end with the percentage of debt to Gross Domestic Product (GDP). Forty years ago the national debt was under 30% of GDP and peaked at just over 40% during the Reagan years. Today, it is well in excess of 100%. That’s correct. This nation’s current debt (I won’t even touch on our future obligations) is more than its annual output of goods and services.

Yet every says, ‘it’s not my fault.’

But make no mistake, every congressman, every senator, and every chief executive for the last 40 years had their hand in this. Did a single politician tender his or her resignation over this? Did anyone in Congress or the Senate stand up and say, “I can no longer be a part of this?”

Our savings accounts have simply become vehicles that do nothing other than waive the fees on our checking accounts. We continue to earn a farcical one tenth of one percent on what you manage to put aside. And they are the reason.

It takes a big hole to trap a leviathan. And the Federal Government has dug theirs pretty deep. Interest rates can’t go up. The theater of the Federal Reserve’s board of governors’ quarterly meeting has become as predictable as Nancy Pelosi’s re-appointment to the House leadership. Near-zero percent rates are all that stands between us and economic chaos.

Is there a way forward?

The United States taxpayer is already on the hook for 20 trillion dollars. The interest on debt alone for fiscal year 2017 takes up 23 billion dollars of the federal budget, and that’s at the current near-zero interest rates. Raising interest rates to make savings attractive again will put service to the national debt at a level which will collapse the economy on an apocalyptic scale. I don’t care how many illegal aliens you get paying into Social Security. There just aren’t enough man-hours of available labor to convert into the required capital.

Our options are limited if we want to avoid economic collapse: devaluation or austerity. Neither one is good, but it’s better than the alternative. We have a new president coming into office, and both houses of congress firmly in the hands of what is supposed to be “the party of fiscal responsibility.” What they do remains to be seen.

I am fortunate enough to have been able to sem-retire at 55 and with a Pension. Also mad some money in Real Estate which was supposed to happen according to the American dream. I spent most of my working career in management and we had no Unions. While in management, Unions did attempt to organize among workers on two separate occasions. Neither try was successful in part because the company ownership was against the idea of any group of workers forming as a Union. Berkshire Hathaway, which once owned 51% of the little Gecko purchased 100% of our company sometime in 1996. We were now a part of the Warren Buffet empire. The Union threats suddenly ended. Not sure why? The next step by Mr Buffet, was to eliminate the Pension Plan for all new associates. Lucky me because I was grandfathered into the old system. What about the new folk? Profit Sharing was the answer (we already had that) for everyone. This works as long as the company makes a profit which is something that does not (ask State Farm and Allstate) really happen anymore. Bottom line is that workers today at my old company are now owned by a guy who supported Hillary while denying Unions and Pension plans. This Hillary whose party kisses up to Unions who still have Pension plans. Somehow I got lost in all of this chatter. Did you mention Dodd-Frank? How can a nice semi-retired guy like me lose his shirt in 2008 because of two Democrats and a Republican President who lost his own vision (if he ever had one) for our country. Maybe we will talk about that at another time.

Amazing insight, Jim. Thank you!

> Our options are limited if we want to avoid economic collapse: devaluation or austerity.

You overlook the possibility of repudiation, which is what will ultimately happen. Debts that can’t be repaid won’t be repaid.

I do mention default here as a possibility, but overall I don’t see it as likely. But we can agree to disagree. Good feedback.